ABSTRACT

Research is ongoing about how investment in paid media and digital owned media drives changes in brand sales. The advertising-intensive curve (Jones, 1990) suggests that paid-media investment is correlated to brands' market position in the repeat-purchase packaged-product category. Building on that framework, the authors analyzed 838 brands in 14 product and service categories for share of spend in paid media and share of digital owned media—unique visitor traffic and traffic to social media—taking into account their relationship with share of sales. Investment in digital owned media was correlated to brands' long-term sales growth rates and to the balance between paid-media and owned-media investment.

MANAGEMENT SLANT

At a macro level, “share of digital owned media to share of market” corresponds to the “share of paid media to share of market” mapped out in past studies.

The effectiveness of digital owned media is influenced by the long-term trend of brand sales and the balance between paid media and owned media.

There is synergy between paid and digital owned media that varies in effectiveness by category and in effectiveness of paid and owned media.

When brands that invest less in paid media shift more of their marketing efforts to owned media, both owned media and paid media will influence sales.

INTRODUCTION

The surge in digital platforms in the 21st century has disrupted the media-spend equation. That disruption has prompted questions about how brands' investment in paid and digital owned media affects brand sales. “Paid media” refers to media activities that a company or its agents generate and pay for. “Owned media” refers to activities that a company or its agents generate in channels it controls—for example, a blog, a website, or a Facebook page.

The advertising-intensive curve (AIC; Jones, 1990), which relates market share to advertising share of voice, demonstrated that paid-media investment is correlated to the brands' market position in the repeat-purchase packaged-product category. Advancing the concept of advertising intensity, researchers since then have explored advertising elasticity and sensitivity for the effectiveness of media investment in product categories, such as consumer packaged goods, telecommunication, and automotive.

The current study expands the approach to review brands' paid media and owned media, using brands' actual expenditure and traffic of the brands' websites and presence on social-media platforms. Analyzing 838 brands in 14 product and service categories, the authors examined the synergy between (or interactions of) paid media and owned media. In that context, the two components were more effective together than either component alone. The study identifies differences in how the synergy correlated to paid and owned media in the various categories.

LITERATURE REVIEW

Paid Media and Owned Media

Professionals in advertising coined the terms “paid,” “owned,” and “earned media” as three categories for the brand activities in offline traditional media and online digital media. Paid media are “media activity that a company or its agents generate,” such as television or radio. Owned media are “media activity that a company or its agents generate in channels it controls.”1 Common examples are a company's website and its official social-media page.

Earned media are “media activity that is generated by other entities such as customers,” such as word of mouth (Stephen and Galak, 2012). Marketers have examined the relationship between paid and owned media. Some found that the content in paid media could direct consumers to owned media.2 Others demonstrated the combined effect of social interactions and television in creating an earned audience (Nagy and Midha, 2014). Owned media also add touchpoints to the paid media and increase brand recall (Harrison, 2013). The current study focuses on paid and owned media with the brand-level data and explores their effectiveness on sales and how they work together.

Advertising-Intensity Curve

The relationship between advertising spend and relative market position or market share long has been a concern for marketers. “Is an advertiser spending the right amount to generate optimum sales and maximum profit?” is the fundamental question.

A 1990 study attempted to provide a general answer (Jones, 1990). Using survey methodology, the investigator collected worldwide brand and advertising information for 1,096 advertised brands. He compared a brand's market share with its share of voice—that is, the total value of a brand's advertising in comparison with the total media value in the category. Examining the difference between market share and share of voice showed that some brands appeared to overspend—that is, the share of voice was higher than the market share—and, of course, some brands appeared to underspend.

The AIC is a plot between the share of market and the difference between a brand's share of voice and market share. The curve shows that brands with higher market share tend to underspend, whereas brands with lower market share tend to overspend. This is a convenient and time-tested budgeting framework for traditional paid-advertising media. The relationship between share of voice and share of market has been a key reference in advertising-budget decisions, indicating a benchmark for advertising spending in a product category for brands to maintain or change their advertising spending (Pringle and Marshall, 2011). The difference between share of voice and market share later was termed as “extra share of voice” (Binet and Field, 2007).

Two metrics were examined as different perspectives to explain the relationship indicated by the AIC:

Advertising elasticity, which is defined as the percentage change in sales or market share divided by the 1 percent change in advertising, has been used to evaluate the effectiveness of advertising (Assmus, Farley, and Lehmann, 1984; Sethuraman, Tellis, and Briesch, 2011; Tellis, 2009). These studies found that larger brands tended to have smaller advertising elasticity, which confirms the conclusion in prior research (Jones, 1990) of advertising economy of scale.

Sensitivity, which is measured as the effects of changes in market share on changes in advertising, has been used to evaluate the effects in fast-moving consumer-goods product categories (Hansen and Christensen, 2005).

The empirical research has led to two competing explanations for the AIC pattern:

Larger brands can afford less spending on advertising without losing market share.

Larger brands invest less in advertising because of the lower advertising elasticity (Danenberg, Kennedy, Beal, and Sharp, 2016).

RESEARCH QUESTIONS AND HYPOTHESIS DEVELOPMENT

Enter digital media, which, no doubt, affect the framework. The idea of owned media is a relatively recent development and has spawned considerable speculation as to how to manage both paid and owned media in a marketing program.3 Previous studies have examined the AIC with media investment on offline media and Internet media, using aggregated data from survey or field experiments, but social media have been considered less. The past studies, moreover, are constrained to categories such as consumer packaged goods, telecommunication, and automotive.

The goal of the current study was to expand the AIC concept to accommodate owned media and move beyond speculation in various product categories. The study defined the traffics in owned media of a brand to the total value of the traffics in the category as share of owned media. Extra share of owned media is the difference between share of owned media and market share.

A secondary goal was to base the analysis on real data, rather than on survey data. The past studies led the researchers to pose the following questions:

RQ1 Does the AIC curve fit the relationship between the extra share of paid media and the share of sales of all product categories?

RQ2 Does the AIC curve fit the relationship between the extra share of owned media and the share of sales of all product categories?

RQ3 What are the differences between the effectiveness of paid media and the effectiveness of digital owned media of all product categories?

Research has found that the relationship between share of voice and share of sales changes under a number of conditions. One study assessed how different types of markets could affect the AIC and found product categories, and how competition in the product categories could influence patterns of the curve (Hansen and Christensen, 2005). Brands in high-voice markets, furthermore, followed the norm and kept investing more to increase share of voice than brands in the low-voice markets.

Other studies confirmed that in media outside of television, AIC changed among different categories other than consumer packaged goods (Danenberg et al., 2016). The relationship also varied by brands' sales-growth rate, because the successful growing brands tended to have less extra share of voice.4 The current researchers thus hypothesized the following:

H1 The effectiveness of digital owned media is shaped by categories, the long-term trend of brand sales, and balance between paid media and owned media.

Multimedia Synergy

Going beyond how brand sales react to the owned media and paid media, respectively, the current study further examined how paid and owned media work together: the synergy effects across multiple media platforms. As the media ecosystem changes today, consumers use a multitasking approach for information across different media channels, such as television and mobile (Schultz, Block, and Raman, 2012). Brands also keep increasing investment in multimedia channels and aim to find a combination of media channels in budget optimization. It therefore is necessary to assess the media investment at an intermediate level. In keeping with the theory of integrated marketing communication, the study examined the simultaneous cross-media synergy effect from paid media and digital owned media.

Synergy is defined as “the joint impact of multiple media that exceeds the total of their individual parts” (Assael, 2011). One author reviewed and reported a growing body of research that emphasized cross-media synergy, and he compared it to what he termed the silo approach, which examines one media channel at one time (Assael, 2011).

The previous research has provided important insights into media synergetic effects. A classic study found that budget should be allocated to the less-effective or even zero-effectiveness media, because they will reinforce the most-effective media (Naik and Raman, 2003; Raman and Naik, 2004). This study was limited to the offline media, however. More recent studies, which integrated the synergy between the offline and online media, found the following:

Television and web advertising worked better together than alone (Chang and Thorson, 2004).

Online advertising enhanced the effectiveness of and synergies among the offline advertising in television, print, newspaper, and magazine media (Naik and Peters, 2009).

Most studies, however, are limited to a few categories, such as fast-moving consumer goods and automotive. Fewer studies have looked at the simultaneous effects of paid media and owned media across the traditional offline media, web, and social-media channels together.

The current study fills a gap in the body of knowledge by examining the synergetic effect among more categories. It also analyzes how paid and owned media effectiveness are related to the synergy. On the basis of the previous studies, the study asked the following questions:

RQ4 What are the combinations of media that generate synergy?

RQ5 How is the effectiveness of paid and owned media varied by the cross-platforms synergy?

METHODOLOGY

The researchers observed the relationship between paid and owned media and sales across 838 brands in the U.S. market. The brands represented 56 subcategories (including credit cards, Internet service providers, cosmetics, and department stores) within 14 categories (including financial services, telecommunication, beauty and personal care, and retail; See Appendix 1). The outcome measurement was brand sales.

The research team collected 5-year sales data (2010 to 2015) from the Bloomberg Terminal, Euromonitor, and companies' IRS Form 10-K. The brand investment in paid media was measured by the actual advertising spending on six platforms: television, radio, outdoor, print, Internet, and search. The brands' investment in owned media was measured by the traffic from their official websites and social-media pages.

Paid-media input metrics—media spending on the six media platforms above—came from Kantar. Owned-media input metrics—unique visitors to brands' desktop and mobile sites—came from comScore, Inc. The other owned-media input metrics—fan acquisition and interactions on companies' social-media sites (Facebook, Twitter, YouTube, and Instagram)—were collected from Publicis Media's SocialTools. (Publicis Media's Social Tools product constantly monitors more than 100,000 brands' social sites across Facebook, Twitter, YouTube, Instagram, and LinkedIn, collating consumer-interaction data from basic fan acquisition to detailed engagement and interaction data.) Access to Euromonitor, Kantar, and comScore were provided through Publicis.

The researchers used the following methodologies:

AIC;

ordinary-least-squares (OLS) regression;

decision tree (chi-square automatic interaction detector [CHAID]);

ridge regression;

K-means cluster analysis.

The AIC (Jones, 1990) was used to review the correlations between

market share and extra share of voice (extra share of voice = share of voice – market share), and

market share and extra share of owned media (extra share of owned media = share of owned media – market share).

Following the original variables in the AIC, the researchers calculated share of voice of each brand, by using the total annual media spending of 2014 and dividing by the brand's subcategory sum of paid-media spending. The researchers calculated share of owned media by aggregating the metrics of desktop and mobile unique visitors, number of fans, and interactions in social media of each brand, and dividing the sum by the brand's subcategory sum of owned-media metrics. The market share was calculated as a brand's annual sales divided by the brand's subcategory sum of sales.

The researchers conducted OLS regression to examine the effectiveness of owned and paid media across all 14 categories and within each category. They calculated advertising elasticity and sensitivity to examine and explain the effectiveness of paid and owned media.

(1)

where ESOV is extra share of voice, ESOO is extra share of owned media, and SOM is share of market.

(1)

where ESOV is extra share of voice, ESOO is extra share of owned media, and SOM is share of market.

In keeping with methods from the previous studies, the authors calculated two metrics—elasticity (Sethuraman et al., 2011) and sensitivity (Hansen and Christensen, 2005)—by transforming the AIC equation:

(2)

(2)

(3)

Brands with larger elasticity have 1 percent change in share of voice or share of owned media correlated with larger changes in market share than brands with small elasticity. Brands with larger sensitivity tended to have 1 percent change in market share correlated with larger changes in share of voice or share of owned media to follow up with the market. Brands with higher elasticity had lower sensitivity.

(3)

Brands with larger elasticity have 1 percent change in share of voice or share of owned media correlated with larger changes in market share than brands with small elasticity. Brands with larger sensitivity tended to have 1 percent change in market share correlated with larger changes in share of voice or share of owned media to follow up with the market. Brands with higher elasticity had lower sensitivity.

The researchers further identified what combinations of media bring synergy by using CHAID, a method introduced to study synergy. They defined synergy as a statistical interaction among two or more media variables (Schultz et al., 2012). A previous study showed that CHAID is a reliable method to detect synergy (Schultz et al., 2012). CHAID adopts a stepwise process to divide the data by a set of predictor variables with respect to the criterion variable—in this study, brands' market share.

The splitting of input variables marks the identified greatest difference. In model visualization, the parent node is split into two child nodes. Each child node becomes a parent and is split again. Interaction is identified as two or more splits having occurred (Schultz et al., 2012).

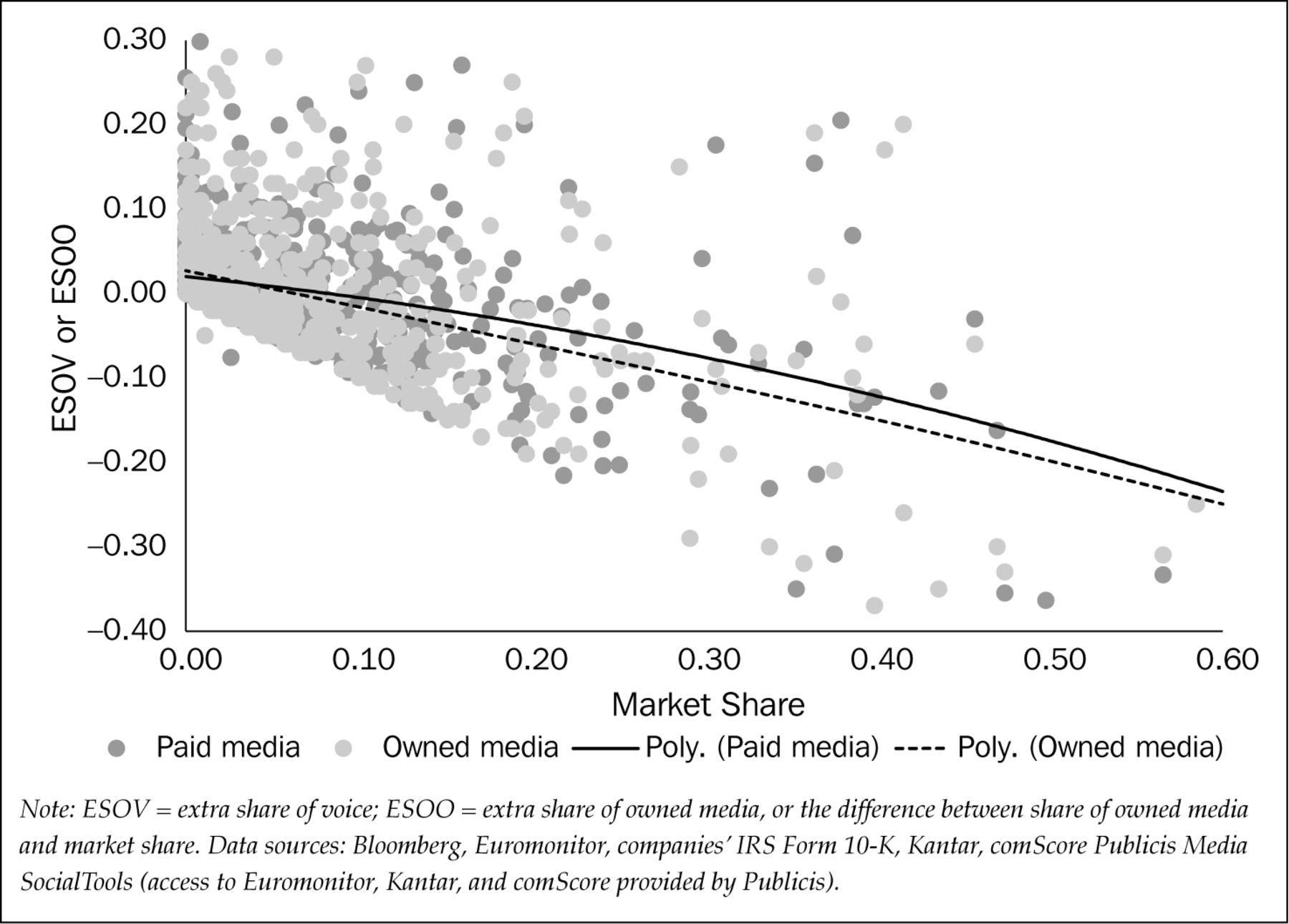

Paid-Media and Owned-Media Intensive Curve: All Product and Service Categories in 2014

Coefficients (β) of Two Simple Regression Models

With a combination of synergetic media identified, the current researchers conducted multiple regressions by the level of one subcategory, using ridge regression to avoid multicollinearity. A detailed discussion of the statistical methods can be found in The Elements of Statistical Learning (Hastie, Tibshirani, and Friedman, 2016). The current researchers then did a K-means cluster analysis, using all the coefficients from the ridge regression (See Appendix 2) as input variables, to partition product subcategories into clusters, and to investigate how synergy worked in different categories.

RESULTS

The researchers conducted two regression models (Model 1 and Model 2) to compare the effectiveness of paid media and digital owned media, addressing Research Questions 1–3. A total of 796 brands were analyzed, after the exclusion of 42 observations with missing values.

For overall categories, brands with smaller market share tended to have their share of voice and share of owned media exceed their market share, whereas brands with larger market share tended to have their share of voice and share of owned media lower than the market share. AIC, therefore, fits the relationships between extra share of voice and market share and between extra share of owned media and market share. The advertising elasticities for both paid and owned media reduced as a brand's market share increased. This indicates that the big brands still can maintain the same market share as they reduce the share of voice and share of owned media to below the levels of their market share (See Figure 1).

In overall categories, as sales grew by 1 percent, brands needed to increase share of voice by 0.61 (1 − 0.39) percentage point and needed to increase share of owned media by 0.53 (1 − 0.47) percentage point to stay with the market benchmark. Owned media had smaller sensitivity and higher elasticity than paid media. The effectiveness of owned media was larger than that of paid media (p = 0.02, z =2.37; See Table 1).

The researchers used OLS multiple regressions to examine whether the effectiveness of paid media and digital owned media was shaped by product and service categories and to examine the long-term trend of brand sales and the investment of paid media (Hypothesis 1). A third model (Model 3) identified the categorical difference in the effectiveness of owned media, although the difference was not statistically significant. (The statistical insignificance could be related to the smaller brand size within a category.)

The Effectiveness of Owned Media of Each Product and Service Category

In Model 3, elasticity demonstrated the effectiveness of owned media, which was calculated from coefficients. Owned media effectiveness was higher in the durable home-goods category than in other categories, followed by automotive and by beauty and personal care. The least effective product categories were retail, travel, and telecommunication (See Table 2).

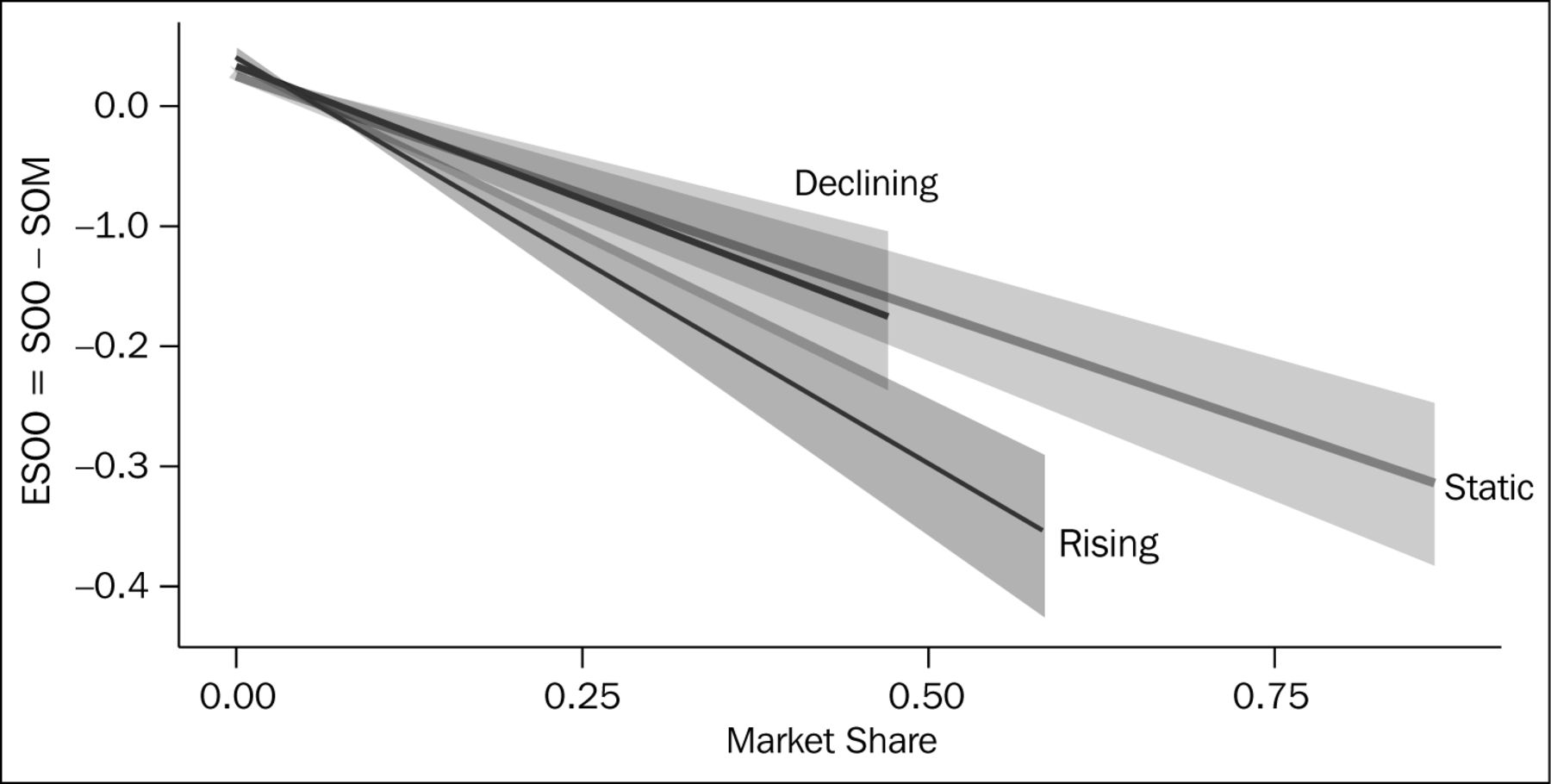

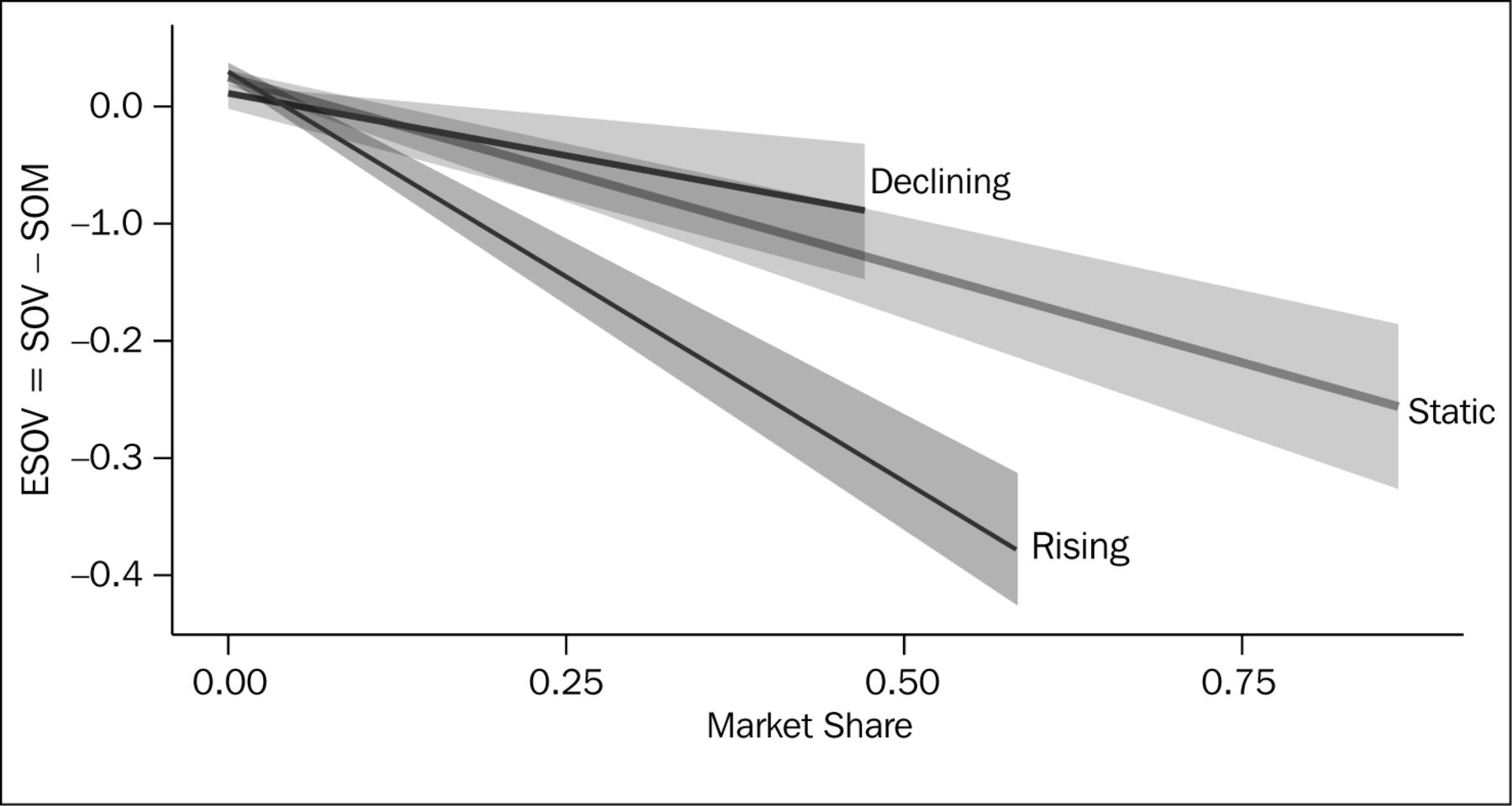

The researchers looked beyond the product categories to see how the effectiveness of paid media and owned media over the long term varied by brands with long-term sales-growth rates. Brands were divided into three groups—rising, static, and declining—depending on their 5-year compound growth rate of annual sales. Brands with market share that decreased by more than 3 percent were coded as declining brands; brands with more than 3 percent market-share growth were coded as rising brands. The rest were coded as static brands.

The authors conducted Models 4 and 5, which included 576 brands with complete 5-year sales, to compare the slopes of the AIC. Rising brands tended to have the least sensitivity and most elasticity. They also were more effective in paid media and owned media than the static and declining brands, although the difference was not statistically significant (See Table 3). As sales grew, the rising brands invested less share of paid media and share of owned media than the static and declining brands did. Declining brands had the most sensitivity, least elasticity, and least effective paid and owned media (See Figures 2 and 3 for a visualization of the regression). As expected, therefore, the effectiveness of paid and owned media varied by the long-term sales growth of brands (See Figures 2 and 3).

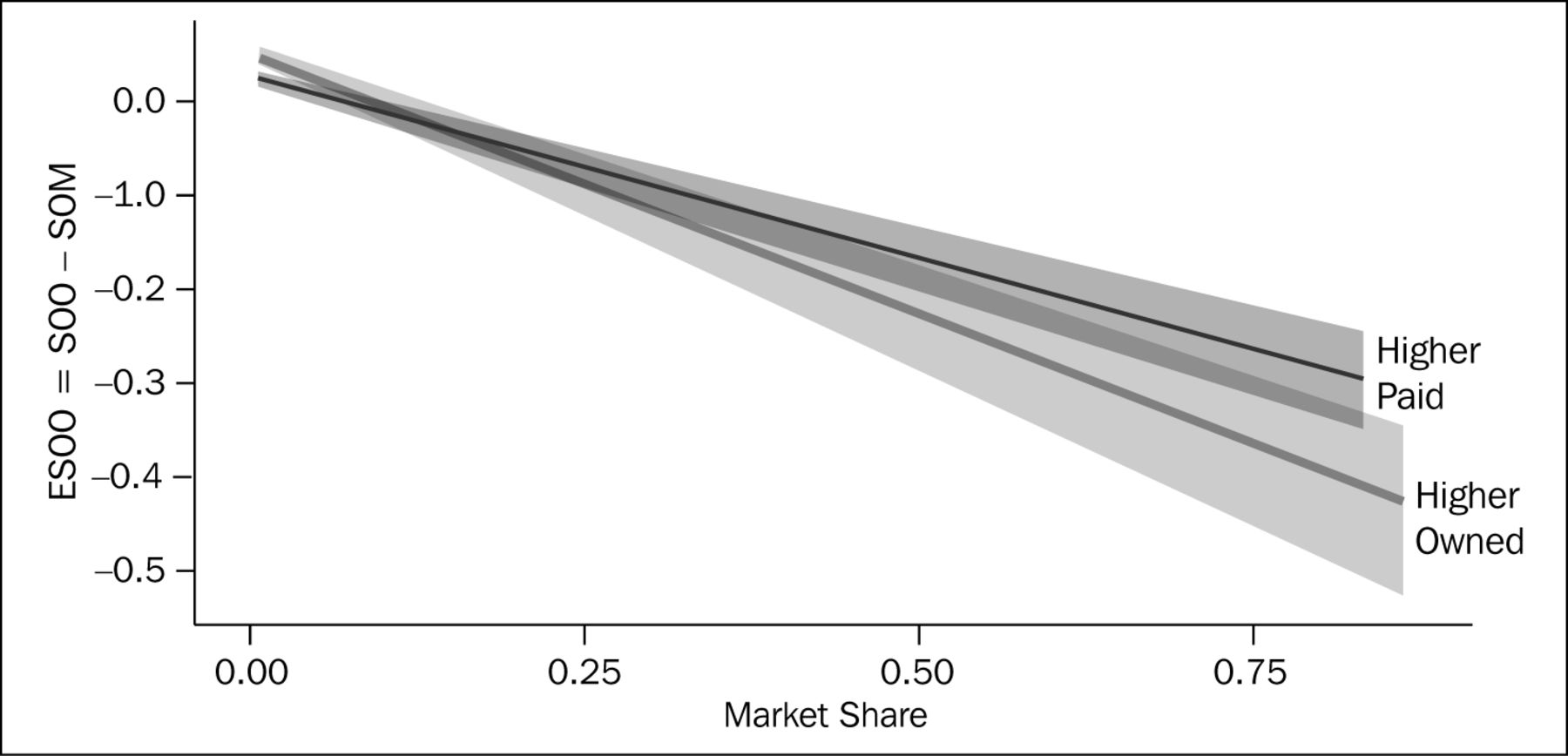

Models 6 and 7 compared the effectiveness of paid media and owned media by the contrast between the two. Brands were divided by different balances between paid-media and owned-media investment:

Brands were ranked by the percentile of paid-media spending and owned-media metrics, respectively.

Brands with paid media that ranked higher than owned media were coded as the higher paid category; brands with owned media that ranked higher than paid media were coded as the higher owned category.

Brands with missing values were excluded from the two models.

Comparing the slopes of AIC, the researchers observed that owned media and paid media were more effective for brands with higher owned media than for brands with higher paid media, because they had lower sensitivity and higher elasticity than brands falling in the higher paid category (See Table 4). As hypothesized (H1), the effectiveness of paid and owned media was shaped by the balance between paid media and owned media. For brands that invested less in the paid media and more in the owned media, both owned media and paid media worked more effectively. (See Figures 4 and 5 for the graphical comparison between paid and owned media in the higher paid and owned categories.)

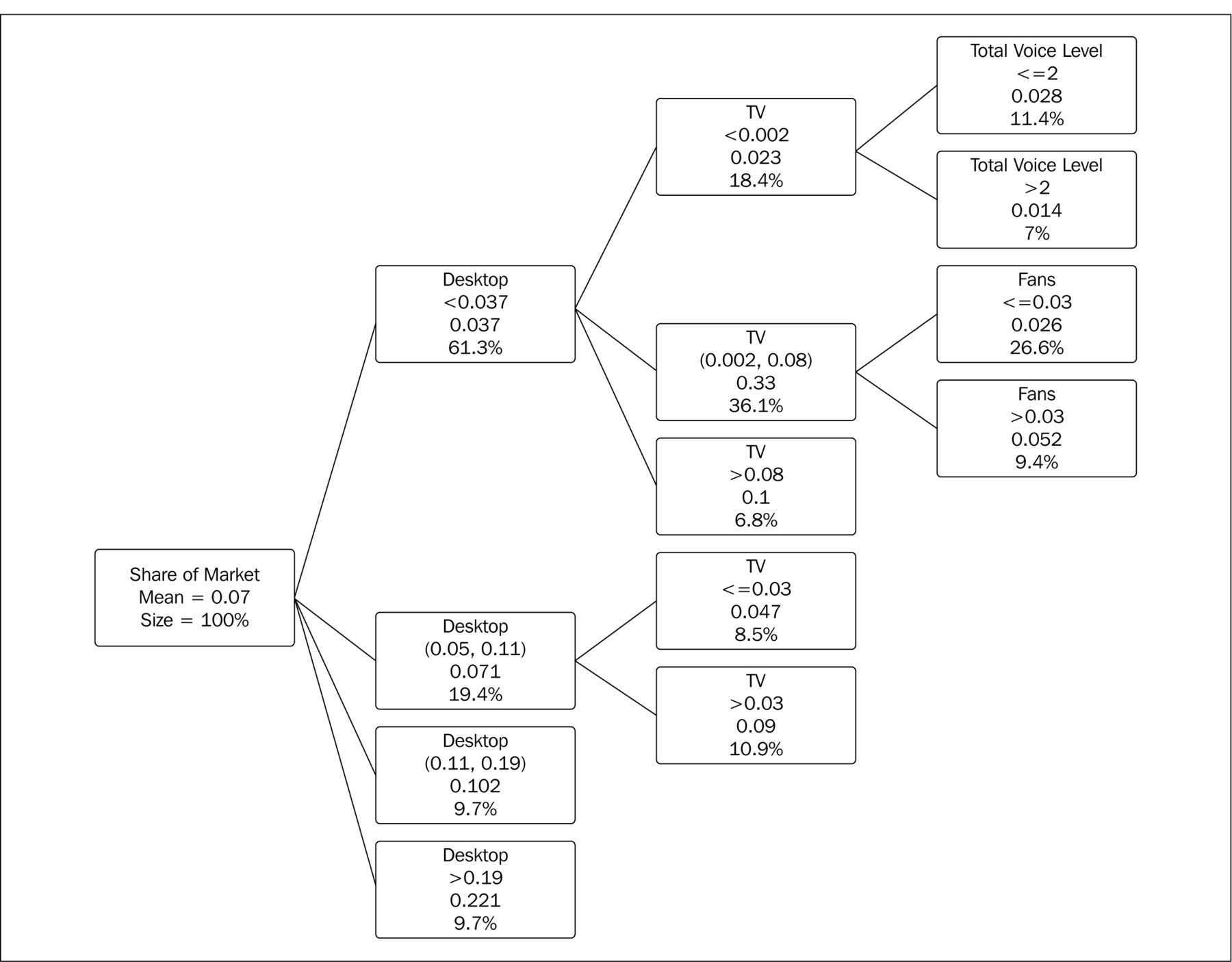

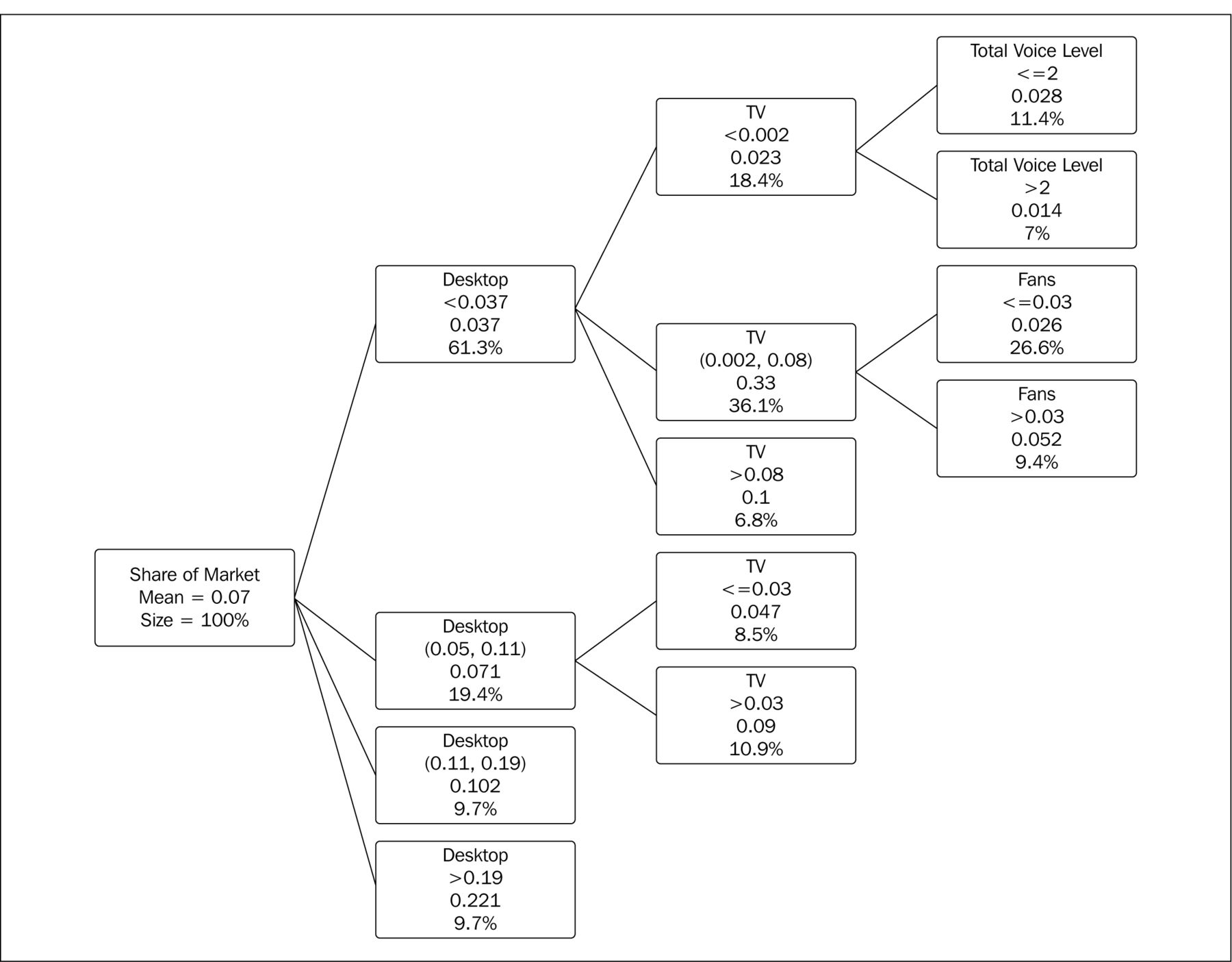

The researchers further examined the combined effect between paid media and owned media, which was defined as synergy in this study (Research Question 4). They applied CHAID to the data, with metrics measuring investment in all the media platforms as input variables and the market share of 2014 as the outcome variable. The analysis found that paid media and owned media worked more effectively together than alone.

The Effectiveness of Owned Media and Paid Media by Levels of Long-Term Sales-Growth Rate

Owned Media of Rising, Static, and Declining Brands

Paid Media of Rising, Static, and Declining Brands

The dependent variable was market share expressed as a proportion, as shown in the parent node as .07, or 7 percent market share (See Figure 6). The size of the node was shown as a percentage; 100 percent represents the 794 brands (excluding 42 brands with a missing value). The first child node (lower left in Figure 6) shows desktop share as less than 5 percent, with a market share of 3.7 percent, representing 61.3 percent of the total brands. The variable that explains the greatest variance enters the equation first and is then followed by the one that explains the greatest variances in the next area. The second and later splits in the decision tree show the different types of combined effects among variables.

The tree plot offers a visual display of the combined effects that exist between television and desktop unique visitors and three-way interactions among television, fans, and desktop (See Figure 6). The predictor explaining the greatest variation was share of desktop. For the two groups with share of desktop unique visitors between 0 and 11 percent, which was about 80 percent of the overall brands, the interaction was between television and desktop. The next most important predictor was share of television. The interaction was between television and fans.

The Effectiveness of Owned Media and Paid Media by Higher Paid and Higher Owned Brand Categories

Paid Media in Higher Paid and Higher Owned Categories

The next question involves the effectiveness of paid and owned media by the cross-platform synergy (RQ5). A straight-forward way of characterizing product categories is to use regression to predict market share within the category from the share-of-voice variables, then use the standardized regression coefficients as characteristics of the category. Two problems emerged: overspecification and collinearity. The share-of-voice variables were intercorrelated, averaging around 0.7. A solution to this problem is ridge regression and the application of a penalty coefficient.

Some product categories had a small number of competing brands; the average was just over 14. The categories with fewer than five competing brands were eliminated from the analysis, which left a total of 50 subcategories. Subcategories eliminated were e-retailers, big-box retailers, warehouse clubs, over-the-top streaming services, prescription drugs, and gaming hardware.

To limit the number of variables into multiple regression models, the authors selected television spending as one variable to represent the paid media, and they used desktop share to represent owned media. Television and desktop, and television and mobile, were combined into an overall interaction term.

Television share of voice, for example, showed a positive coefficient between television share of voice and market share (.09). The highest product and service subcategory for television share of voice, at .65, was tablets, followed by beer, television and Internet service providers, cereal, wireless carriers, and quick-service restaurants.

The K-means cluster analysis showed that all the categories were clustered into two groups, labeled “low synergy” and “high synergy.” The high synergy shows that the effectiveness of the synergy between television and digital owned media, on the one hand, and market share, on the other, was as high as 1.11. In contrast, the effectiveness was only 0.30 in the low-synergy cluster. That means in the high-synergy group, television, brand sites, and social media worked jointly more effectively to market shares. In the high-synergy group, the effectiveness of television spending was as high as 0.13, compared with 0.08 in the low-synergy group. The effectiveness of the digital owned media was almost the same.

Owned Media in Higher Paid and Higher Owned Categories

Brands of Low Synergy and High Synergy

The high-synergy product subcategories included beer, cars and trucks, casualty and property insurance, cereal, fragrances, pet food, video games, and wireless carriers. They were mostly from higher paid categories, with higher consumer interactions in social media and higher traffic in brands' mobile sites.

The low-synergy product subcategories included television and Internet service providers, department stores, supermarkets, yogurt, bottled water, casual dining, computer hardware, and cosmetics. They mostly had higher digital spending and higher traffic in brands' desktop sites.

DISCUSSION

The current study found a relationship among paid media, digital owned-media investment, and the brand's market position. It examined the effectiveness of paid and owned media across various product and service categories by adopting the AIC method.

As a brand's market share grew, the researchers observed, the share of voice and share of owned media tended to be lower than its market share. The effectiveness of share of owned media and paid media was related to product categories and subcategories, the long-term sales change of the brands, and the balance of paid media and owned media. The study further examined the cross-media synergy, considering paid and owned media working together.

The researchers believe their work has advanced the concepts and mechanisms of advertising intensity by applying it under different contexts. First, the study confirms that the advertising intensity showed a similar pattern for the relationship between sales and owned media. Second, the findings suggest that the paid media and owned media effectiveness were shaped not only by the product categories but also by the balance between paid and owned media and a brand's long-term business performance.

Brands that were growing and that weighted more investment to owned media tended to have both paid and owned media work more effectively than the rest. When paid and owned media were working together synergistically, investment in television advertising tended to interact with consumer behavior in social media and the brand websites. In higher synergistic subcategories, television worked more effectively than in lower synergistic subcategories.

IMPLICATIONS AND LIMITATIONS

In terms of practical implications, the current study found that when brands allocated media investment in paid and owned media, more investment was not always consistent with more market share. This is consistent with suggestions by previous researchers (Danenberg et al., 2016). The current research, moreover, contradicts previous synergy studies that suggested media investment should be allocated to the least effective media, because it would leverage the synergy with the most effective media (Naik and Raman, 2003; Raman and Naik, 2004). As the current authors found, there is synergy across television, web, and social media, and marketers should balance both paid and owned media when making bud geting decisions.

Decision Tree (Chi-Square Automatic Interaction Detector) Detailing Synergy Between Paid and Owned Media

The current study has limitations. First, the researchers used aggregated data rather than single-source data, which can identify unduplicated reach. With aggregated data, synergy may be just additional reach (Havlena, Cardarelli, and De Montigny, 2007; Taylor et al., 2013). Data with cross-media exposure on the same consumer could be more accurate in examination of synergetic effects (Varan et al., 2013; Voorveld and Valkenburg, 2015).

The current authors defend the use of aggregated data because these were the best data of such a large sample of brands—838—that were accessible. The study, moreover, did not imply any causal relationship among owned media, paid media, and sales performance with time-series analysis, as examined by other researchers (Kumar, Choi, and Greene, 2017). Future studies could conduct time-series analysis for the synergetic relation across paid and owned media.

ABOUT THE AUTHORS

Rob Jayson is evp, lead, insights and analytics at the media agency USIM in New York City. He conducted the research when he was global lead, branded applications, at Publicis—one of several leadership positions he has had at major media agencies over the past 25 years.

Martin P. Block is a professor of integrated marketing communications at the Medill School of Journalism, Media, Integrated Marketing Communications (IMC) at Northwestern University. In addition to his academic career, Block has consulted for various companies, including Allstate, General Mills, Hewlett Packard, IBM, Kraft Foods, Miller Brewing, 3M, T. Rowe Price, and Visa International. His work can be found in books he has authored and in book chapters, academic research journals, and trade publications.

Yingying Chen is a doctoral student in information and media at Michigan State University.

APPENDIX 1 Fourteen Product and Service Categories, with 56 Subcategories

APPENDIX 2 Table of Ridge Regression Coefficients

Footnotes

↵1 S. Corcoran. (2009). “Defining Earned, Owned and Paid Media.” Retrieved October 1, 2017, from the Forrester Research Blogs website: https://go.forrester.com/blogs/09-12-16-defining_earned_owned_and_paid_media/.

↵2 R. Bonn. “Making and Keeping the Brand Promise: How Paid and Owned Media Are Stronger Together.” Market Leader, January 2014.

↵3 D. Newman. (2014, December 3). “The Role of Paid, Owned and Earned Media in Your Marketing Strategy.” Retrieved September 11, 2017, from the Forbes.com website: https://www.forbes.com/sites/danielnewman/2014/12/03/the-role-of-paid-owned-and-earned-media-in-your-marketing-strategy/#1bbc1f1428bf.

↵4 R. Whiteford, N. Clarke, and P. Field. (2010). “Why Share of Voice Matters.” Retrieved October 1, 2017, from the WARC website: https://www.warc.com/SubscriberContent/Article/A92885_Why_share_of_voice_matters/92885.

- Copyright© 2018 ARF. All rights reserved.

REFERENCES

Vol 58 Issue 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Jump to

- Article

- ABSTRACT

- MANAGEMENT SLANT

- INTRODUCTION

- LITERATURE REVIEW

- RESEARCH QUESTIONS AND HYPOTHESIS DEVELOPMENT

- METHODOLOGY

- RESULTS

- DISCUSSION

- IMPLICATIONS AND LIMITATIONS

- ABOUT THE AUTHORS

- APPENDIX 1 Fourteen Product and Service Categories, with 56 Subcategories

- APPENDIX 2 Table of Ridge Regression Coefficients

- Footnotes

- REFERENCES

- Figures & Data

- Info